A fair exchange: What Kenyans expect when sharing financial data

A fair exchange: What Kenyans expect when sharing financial data

29 May, 2026 •In January 2026, Tools for Humanity was reported to have deleted sensitive personal data it had unlawfully collected from Kenyans. This followed a High Court ruling and multi-agency investigation into Tools for Humanity’s data processing practices, after it gathered Kenyans’ iris scans and other sensitive personal data in exchange for Worldcoin tokens, which at the time, were worth around KSh 7000 (~ USD 55). This is just one of several high-profile cases testing and enforcing Kenyans’ data protection rights.

It was no surprise then that when asked about attitudes to data sharing, Kenyan survey respondents demonstrated a much clearer sense of ownership of their data than survey respondents from other jurisdictions. This is one finding from surveys conducted in 2025 when Cenfri, in partnership with CGAP and with the support of GIZ, commissioned consumer research in Kenya to understand consumer perceptions and attitudes towards financial sector data sharing.

The research, which is part of our open finance portfolio, found that consumers view data as an asset that can unlock improved financial outcomes, and they base their willingness to share on how they weigh these benefits against perceived risks. This is consistent across income groups and among both individuals and small business owners.

Who owns the data and who controls it?

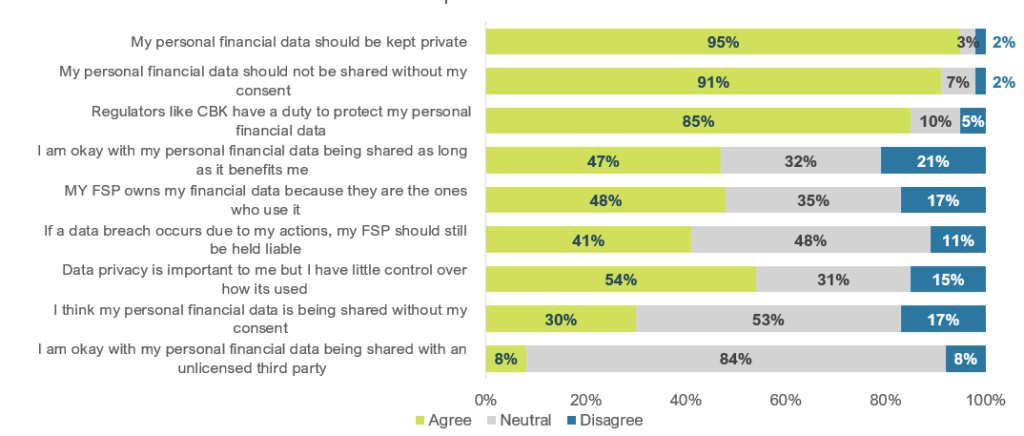

Despite Kenyan consumers expressing a strong sense of ownership over their personal data, this does not translate into a feeling of control over their financial data. Survey responses, as illustrated in Figure 1 below, show how respondents perceive data sharing and its implications.

Most survey respondents (72%) indicated that they believe they own their data. However, 48% reported that once their data is held by a financial service provider, control shifts to the institution. This creates a power imbalance, where providers can determine how, when, and with whom data is accessed, often without the consumer being fully aware or in control. When control becomes opaque, the transaction no longer feels like an equal exchange, but rather one in which influence rests disproportionately with the institution.

Are consumers choosing to share, or just clicking through?

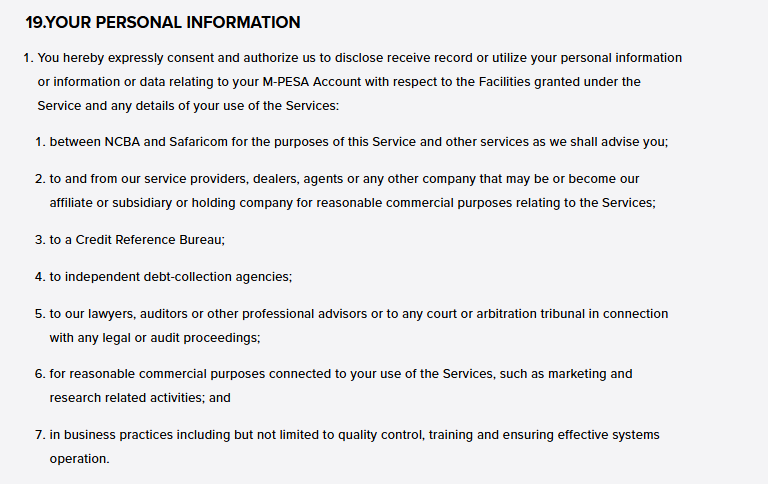

Consent is required to share data, yet it is often not meaningfully informed. Under Kenya’s Data Protection Act (2019), consent must be unequivocal, free, specific and informed, yet in the consumers’ experience, it is often embedded within lengthy and complex terms and conditions that consumers rarely read or fully understand. This makes consent feel passive, weakening a consumer’s sense of control. Figure 2 below shows the personal information sharing conditions of obtaining an overdraft service for a mobile money product in Kenya.

Kenyan consumers articulate this point clearly: “They provide you with so much documentation that you won’t read, you just click.” This does not show indifference, but overload. Consumers distinguish between implied consent and informed consent, expressing discomfort with the idea that agreement is assumed simply because a service is accessed. For them, meaningful consent means understanding what is being exchanged, why it is being shared, and what they stand to gain in return.

What are the benefits of data sharing?

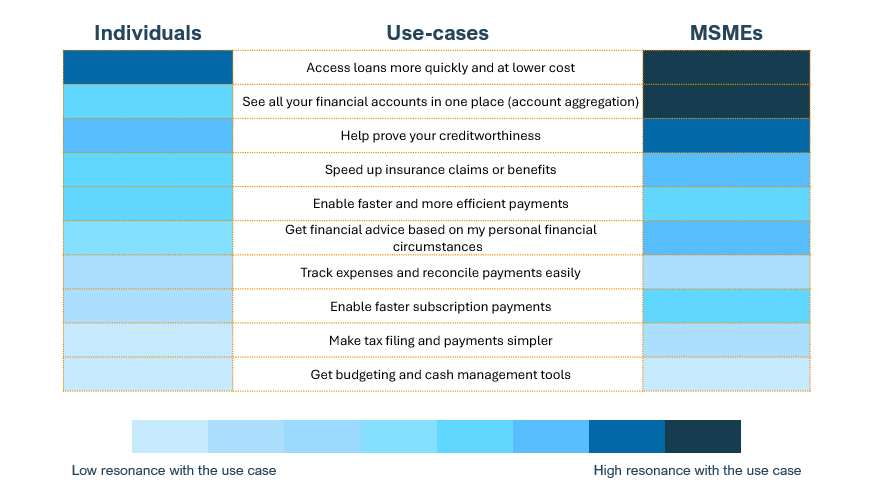

For data sharing to feel like a fair exchange, the benefits must be visible and tangible. Figure 3 below shows the most in-demand data sharing use cases among individuals and MSMEs. These are quicker access to more affordable loans, account aggregation, and tools to better reflect creditworthiness.

These use cases speak directly to everyday financial constraints: the cost of borrowing, the ability to compare accounts in one place, and the opportunity to use existing transaction histories to unlock better terms. However, while many respondents feel that sharing personal financial data is more likely to help than harm, close to 30% remain uncertain about the benefits of sharing their information.

What are the perceived risks of data sharing?

Loss of control over personal data is the biggest concern among Kenyan consumers. Figure 4 below highlights that this is driven by fears of unauthorised access and misuse. The majority of respondents (80%) also indicated that they were unsure whether their information was already being shared without their consent. This can lead to unwanted advertising from third-party providers, as one respondent noted: “I think the fact that someone would give a third party [your information], without your consent, to call you for a loan that you are not interested in or have not requested.” Together, these findings show that perceived loss of control and lack of transparency are key barriers to building trust among consumers sharing data.

What is needed?

The research suggests that Kenyan consumers are not opposed to sharing their data, but the conditions under which it happens matter. However, our research, and an analysis of complaints made to the Office of the Data Protection Commissioner (ODPC) about digital credit providers suggest that to date, data protection principles – such as informed and revokable consent and data minimisation – are not embedded in the financial sector, meaning consumers have not had confidence they were in control of their data.

For open finance to work in Kenya, the system must reflect what consumers say they need to feel comfortable sharing their data. Industry and regulators need to ensure that the following conditions are in place for consumers to comfortably and safely share their data:

- Clear value for sharing their data. Benefits such as faster access to credit, better pricing, or improved visibility over their finances make the exchange feel worthwhile.

- Consent must be simple and meaningful. Consumers are uncomfortable when permission is hidden in lengthy terms and conditions that they are unlikely to read or fully understand

- Control must remain with the consumer. Throughout the data sharing process consumers must have the ability to see when data is accessed and to withdraw permission or revoke consent when they so choose.

If sharing information is transactional, then only a fair and balanced exchange, supported by clear and well-enforced rules, will sustain it.