Can insurance shift incentives around resilience?

Can insurance shift incentives around resilience?

4 August, 2025 •“It’s like robbing Peter to pay Paul”. This quote from a KwaZulu Natal (KZN) municipality captures the cycle many South African municipalities are currently trapped in – scrambling post-disaster to shift funds from maintenance to disaster response.

In 2022, South Africa’s KZN province was hit by catastrophic floods that claimed over 450 lives. The devastation was immense; more than 12 000 homes were destroyed, and the economic fallout was severe, with infrastructure damage amounting to R17 billion[1].

Recently, South Africa’s Eastern Cape province suffered devastating floods that killed over 100 people, displaced 4 000, and affected more than 6 000 households. The floods also caused widespread damage to homes and schools, disrupting education for thousands of students, as well as impacting roads and bridges across the province. [2]

These disasters highlight a troubling pattern: a crisis hits, emergency funds are scraped together, and municipalities rush to fix what’s broken, patching up one part of the system at the expense of another. This reactionary approach focuses on short-term fixes rather than addressing the root causes of vulnerability. The result is a cycle of damage and delayed recovery, with local governments not meeting the needs of the community they serve.

So, how do we change this?

South African municipalities are struggling

South Africa’s 257 municipalities are legally at the forefront of disaster management and response in South Africa, with national and provincial support available for severe events[3]. Many South African municipalities operate under serious structural and financial constraints.

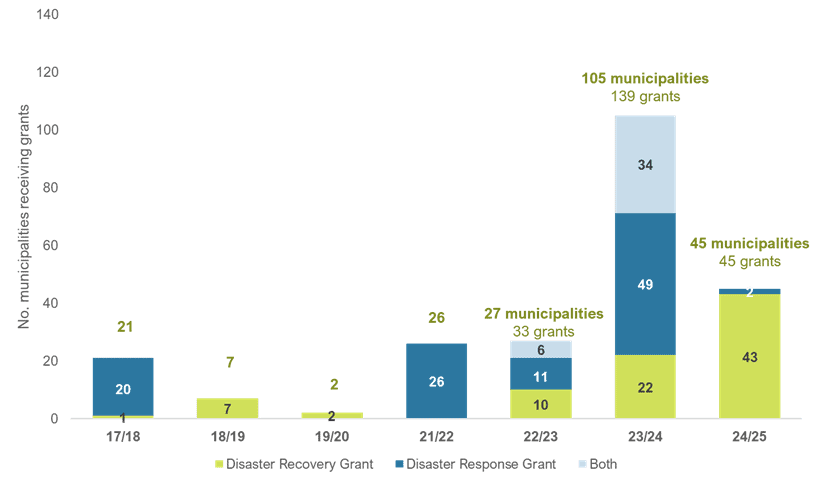

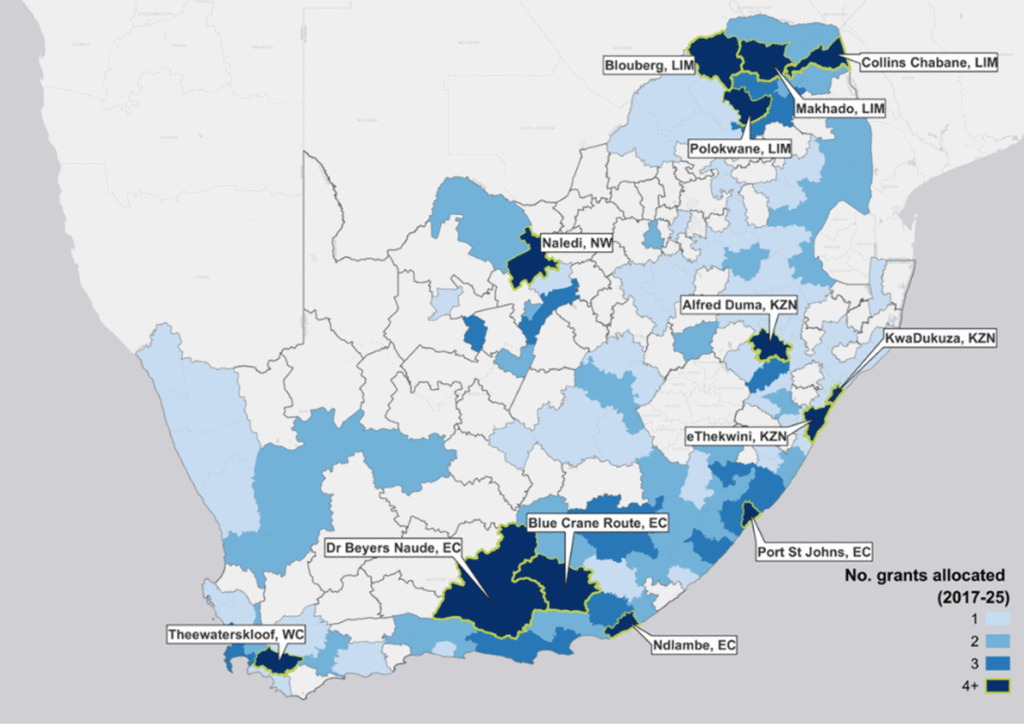

From our study (World Bank, 2025), we found that South African municipalities regularly depend on national grants to respond to and recover from disasters. According to the National Treasury’s data[4], since 2022, over 54% of municipalities have received at least one disaster recovery or response grant, highlighting both their exposure to shocks and their limited capacity to respond effectively.

While the number of grants has increased, delays and uncertainty in accessing these funds undermine their effectiveness. On average, response grants arrive nearly five months after a disaster strikes. And when they do arrive, municipalities surveyed received only around 55% of the funding they applied for, with little clarity on what gets approved or why.

This uncertainty makes it difficult to plan and impacts future resilience. Municipalities delay recovery work because they don’t know if they will be reimbursed, or they shift scarce budgets from maintenance or resilience investments to disaster recovery to deal with critical immediate repairs. When funding finally comes through, limited capacity and compliance or administrative restrictions often lead to under-utilisation.

Insurance: an untapped incentive for disaster preparedness

Insurance could be a powerful tool for disaster risk-financing, yet South Africa faces a significant municipal insurance gap. Based on the interviews we conducted with 26 South African municipalities, only 32% used insurance post-disaster.

While most municipalities were insured, many of them were not insured in a way that helped after a disaster. The problem is not always a lack of insurance but rather having coverage that does not match the risks. When disaster strikes, municipalities are at the frontline, struggling to respond and rebuild.

Based on our research, we uncovered three primary gaps in municipal insurance:

- They’re insured for the wrong things. Municipalities typically ensure laptops, buildings and vehicles and some infrastructure, but not the assets in the open such as roads, bridges, and pipes, etc, which tend to be impacted post-disaster. Why? Assets in the open are considered high risk – particularly when they are old or poorly maintained – making them too risky for insurers to take on.

- They’re insured for the wrong amount. Budgetary pressure and lack of insurance understanding mean that municipalities insure at book value rather than replacement cost. The premium drops, but payouts are insufficient to restore damaged assets or in some cases, claims are not be possible. Prioritising which assets to cover, coupled with a focus on risk reductio,n would be cheaper and would offer better value.

- Claims take a long time. Asset registers are maintained for accounting purposes rather than insurance or risk management. Even where cover is in place, claims often fail or payment takes a really long time, due to a lack of compliance with policy terms. Proper records and risk management can improve claim speed and success but also reduce damage and the need to claim at all.

Rethinking insurance as a tool for change

Municipal budgets are stretched, and capacity is thin, so urgent issues take priority over important, long-term planning. But insurance can shift incentives. Some examples are as follows:

- Inaction turns from risk to cost. When premiums reflect actual risk, they make the cost of inaction visible. Suddenly, not fireproofing key sites, not fixing a flood-prone culvert or ignoring drainage maintenance isn’t just risky, it’s expensive. This can nudge local officials to look for smarter, future-focused choices.

- Capacity and systems to reduce risk. Many municipalities do not have the technical skills to manage risk effectively and often assume insurance covers them regardless, only to find claims denied due to non-compliance. This is where skilled brokers matter: they can help municipalities understand their risks, build systems to manage them, and reduce disaster-risk-related costs. Insurance requirements can even act as an internal lever, giving disaster-risk teams the backing they need to prioritise preventative work.

- Liquidity to recover. Insurance can pay out faster than grants, with more certainty, in instances where proper cover and policy compliance is in place. Swift recovery improves resilience and avoids the need to raid maintenance budgets to cover emergency repairs.

- Longer-term impact. Insurance can offer more than just a payout. By vetting suppliers and managing post-disaster procurement, insurers can mitigate widespread corruption and bring in expertise that rural municipalities often struggle to access.

These benefits may not be automatic since municipalities often treat insurance as a commodity to be procured based purely on the cost of the premium, even if the cover is not fit for purpose. Many municipalities don’t understand the trade-offs, lack the capacity to manage insurance effectively, or simply pass the problem up to national government when things go wrong.

So, what can be done? Municipalities need smarter approaches to procurement and use of insurance, better data and coordination to plan and price for risk. National government should also consider national-level insurance for critical infrastructure to help pool larger risks for affordability of cover, liquidity for response and visibility of local disaster risk. Outside of traditional indemnity cover, parametric insurance can provide cover for catastrophic risk beyond what can be addressed through risk reduction.

Insurance alone is not enough. Grants will remain important to cope with some disasters; and many municipalities are dysfunctional, requiring structural reforms. Operation Vulindlela, the White paper on Local government, NDMC disaster risk management reforms and the Climate Change Response Fund are all key initiatives to improve disaster resilience. Learn more about how this can be achieved in our work on municipal disaster risk finance here.

[1] Santam Insurance Barometer Report (2023)

[2] Eyewitness News (EWN) (2025)

[3] South Africa has three spheres of government: local (municipal), provincial and national. Each sphere owns and is responsible for their own assets including related disaster risk management and response. National response and recovery grants are available to municipalities for severe unforeseeable and unavoidable events. Response grants are for immediate relief and recovery grants for longer term infrastructure recovery.

[4] National Treasury’s DORA (Division of Revenue Act) data was used for this analysis.

[5] The year 2020/21 was excluded because all municipalities received a grant due to the Covid-19 pandemic.