Time for a bold move? The case for renewed zero-rating of low-value mobile money fees in Rwanda

Time for a bold move? The case for renewed zero-rating of low-value mobile money fees in Rwanda

21 September, 2023 •Rwanda must be cashless by 2024 – that’s the bold target set in the National Payment System Strategy 2018-2024.

This policy has strong empirical backing, with a whole range of literature that documents the benefits of digital financial services. Moving from cash to digital payments saves people travel and time costs, makes it easier to access social assistance, helps MSMEs to access new markets, and has been shown to promote women’s empowerment. Having a digital transaction record also makes a consumer or MSME’s economic value visible for credit extension. Furthermore, financial services can boost household resilience, including to climate change– and digital payments are often a gateway financial service to open up access to further services such as savings and insurance. In all of these ways, digital financial services tangibly contribute towards the Sustainable Development Goals:

- In the north of Uganda, households’ use of mobile money accounts raised food security by 45%

- In India, it was found that paying women’s social benefits directly into their own account increased their financial control and incentivised them to find employment, compared to those paid in cash

- In Kenya, the spread of mobile money saw 1 million households – 2% of the population – lifted out of extreme poverty between 2008 and 2014, and M-Pesa helped Kenyan households to improve their resilience to shocks by helping them to draw funds from their informal/social support networks.

- In Tanzania, mobile money users were able to replace two-thirds of the losses incurred due to a rainfall shock with the help of remittances

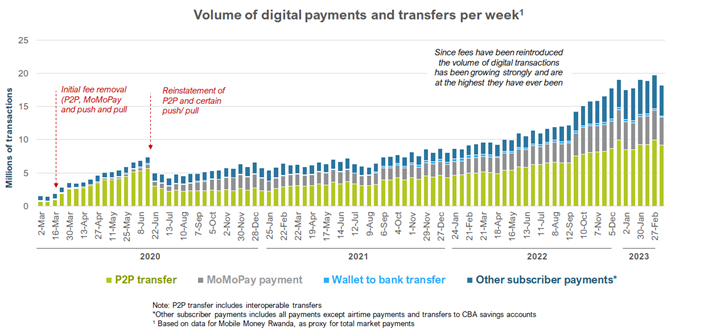

Progress towards a cashless Rwanda has been remarkable, partly triggered by the policy move at the start of the first COVID-19 national lockdown in 2020 to temporarily remove mobile money fees. Almost overnight, transaction volumes spiked. Close to 700,000 new subscribers were added in just three months, many of them women. When fees were eventually reinstated, first for P2P payments and later for merchant payments, volumes did drop again, but not to pre-pandemic levels, and volumes have been on the rise ever since. In March 2023, more than 100 million mobile money-based digital transactions were made.

But with 2024 just around the corner, new actions are needed to reach the target. Our data projections suggest that more than 120 million transactions a month are still done in cash. That’s more than half of all estimated retail payments made in Rwanda, most of them low-value transactions for ordinary families.

We did some in-depth qualitative interviews with merchants, consumers and farmers to help us understand why. It shows that cash is valued because it’s perceived as “free” and is trusted and familiar. It does not require any phone and cannot be interrupted. For those who have digital accounts, but often transact in cash, cash-out fees pose friction. On the other hand, it is acknowledged that digital payment methods provide greater security and facilitate proof of payment and record keeping. It can also allow transfers over a distance. The benefits of digital payments come at a cost, however – a fact that is particularly irksome to merchants. Fees for MTN MoMo Pay (the service to facilitate person-to-business payments to a merchant code) were flagged as a significant deterrent, yet the fees are poorly understood. Merchants do not know how to calculate the 0.5% ad valorem fee levied, leading them to grossly inflate the perceived fee, which they then pass onto consumers.

- “It all depends, it is a fixed amount.”

- “I know on a purchase of RWF25,000, I pay RWF3,500.”

- “I don’t know, I think it is 50%.”

- “I cannot calculate it, because there is not a 0.5% button on a calculator.”

Merchant interviewee responses, November 2021

Ultimately, consumers pay the price, especially in the current high-inflation environment. This creates a strong imperative for fixing the constraints to more entrenched and pervasive use of digital payments – and at the heart of that lies the need to revisit pricing.

The COVID-19 lockdown policies showed just how dramatic the impact of a fee removal on subscriber and transaction volumes can be. It also showed that the rise in volumes soon make up for lost fee income. Can dropping fees again lead to a structural shift in consumer behaviour?

Behavioural science shows that fee interventions are one of the empirically proven ways to influence customers’ financial behaviour. This strategy has been successfully adopted in other countries:

- In Sweden, hailed internationally as a society that has gone cashless, the success of the digital payments drive rests on the convenience and low cost of the Swish mobile-based instant payment platform. All transactions are free for customers.

- In Kenya, M-PESA has adopted a strategy of using the fees from high-value transactions to make up for losses of fees from low-value transactions. Following the temporary reduction in fees during the COVID-19 pandemic, Safaricom announced that it would permanently reduce M-PESA tariffs for lower-value person-to-person (P2P) transactions, affecting more than 90 percent of customer transactions for sending money. All transaction fees below KES100 (~USD 0.7 at current exchange rates), were zero-rated. In January 2023, charges were also substantially dropped for bill payments and other business-to-customer transactions, again on a sliding scale so that low-value transactions benefit most.

What would be the effect of zero-rating low-value transaction fees in Rwanda?

Looking at historical data on P2P and merchant transaction values and volumes, agent commissions, fee structures and fee income, we were able to run a projection scenario that shows that, if P2P and merchant payments below RWF10,000 (approximately USD8.50) in value were zero-rated, P2P volumes per week could double in just a few months (at least five times more quickly than if the status quo is maintained). Moreover, we project that the higher subsequent P2P volumes would see lost fee income be made up over the medium term. Merchant payments may reach their original fee income levels even sooner. And for an average family in Rwanda, such a move means saving at least RWF1,500 a week – a full 5% of their weekly household income. Thus, giving way on fees may result in a win-win situation for consumers, policymakers and market players alike, without compromising the sustainability and innovation of mobile money services.

Perhaps it’s time for a bold move?

Doing so would require careful real-time monitoring of trends to track the upshot and iterate if needed. The foundation of the Rwanda Economy Digitalisation Programme that Cenfri is implementing with the Government of Rwanda and the Mastercard Foundation is to leverage the power of data for decision-making.

This article was originally published by New Times Rwanda.