Why are more women in Africa not making use of digital financial services?

Why are more women in Africa not making use of digital financial services?

23 February, 2026 •This blog was written as part of GIZ’s Governance of Digital Finance project. Blog 1 of 3.

According to the 2025 Findex, women’s account ownership now stands at 77% globally, up from 58% in 2014. This progress matters, as digital financial services (DFS) are shown to enhance women’s economic opportunities and financial resilience.

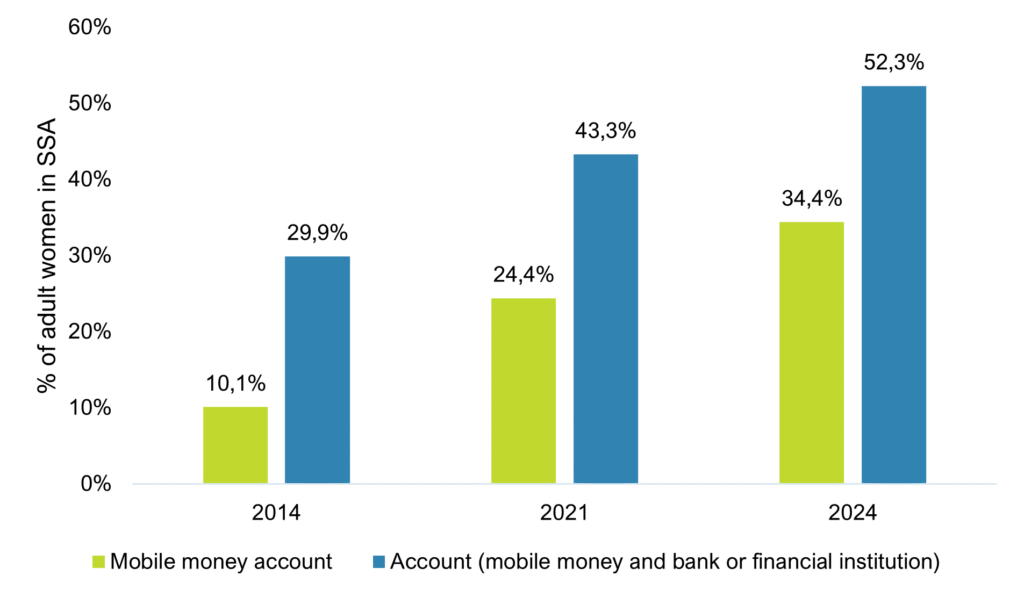

Figure 1 shows how this growth is mirrored in sub-Saharan Africa (SSA), with the percentage of women with any type of account, (including mobile money accounts and financial accounts at banks or similar financial institutions such as credit unions or microfinance institutions), growing from 30% in 2014 to 52% in 2024. A large part of this growth is attributable to the mobile money component – uptake of mobile money accounts among women in SSA increased by 24 percentage points, from 10% in 2010 to 34% in 2024.

In addition to this, women not only have more accounts, but also use them more: 45% of women account owners in SSA had made or received a digital payment in 2024, up from 24% in 2014. Moreover, the percentage of women who formally save through a mobile money account grew from 18% in 2021 to 29% in 2024, an increase of 11 percentage points.

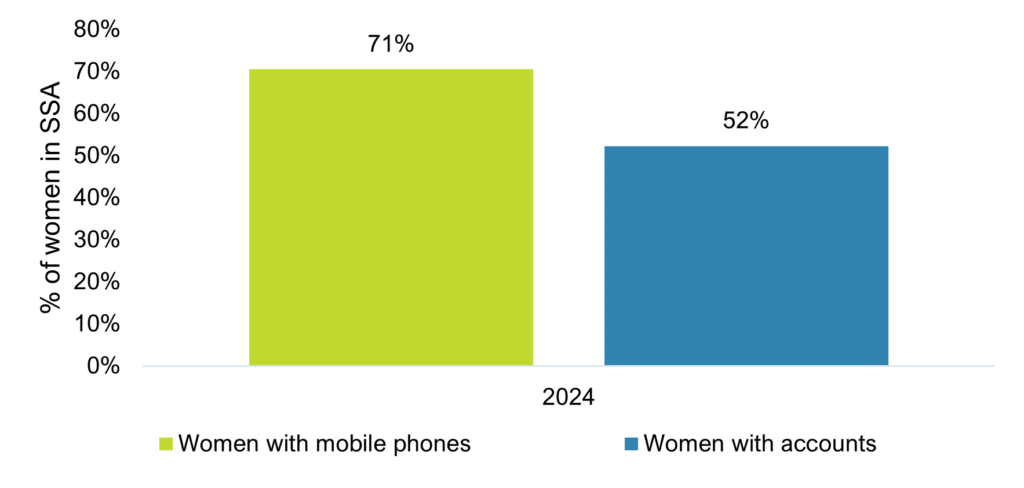

Mobile phone ownership, along with the proliferation of mobile money, has long been hailed as a game changer for women’s access to financial services. Findex’s new Digital Connectivity Tracker corroborates this: as of 2024, 71% of women in SSA own a mobile phone—29% of whom own smartphones. Additionally, average ID ownership rates among women in SSA exceeds 70% according to Findex, which is crucial for phone and account registration.

With high rates of mobile phone ownership and personal identification, many women are able to access digital financial services. However, as Figure 2 indicates, there still remains a significant gap between the number of women with phones and those who actually have accounts:

This gap suggests that mobile phone ownership, by itself, is not enough – there are other sticky barriers that prevent the full potential of digital connectivity from being reaped for women’s inclusion across the continent.

Why the disconnect?

To uncover the reasons behind this, we undertook a further analysis on Findex’s 2025 data by looking at the main barriers to financial account ownership and mobile money account ownership among women.

- Limited affordability and value proposition

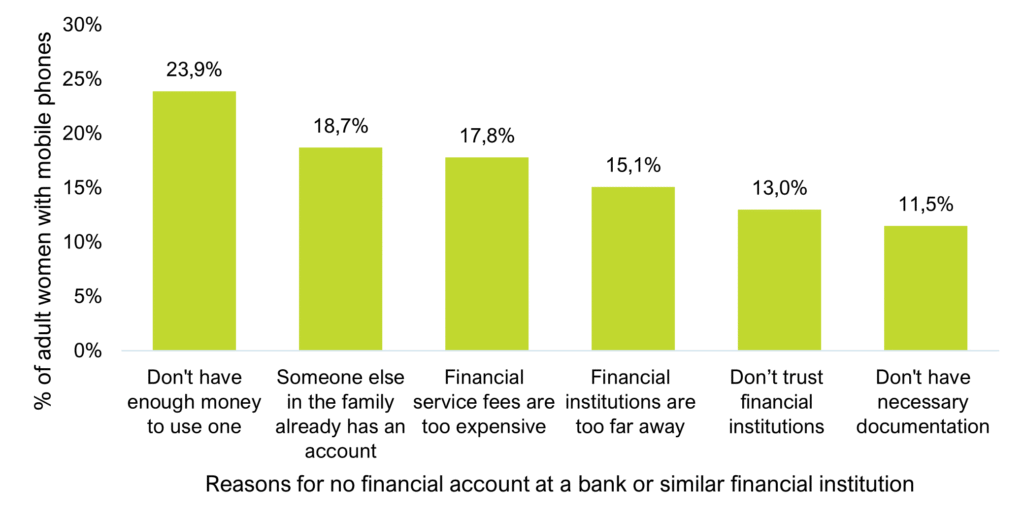

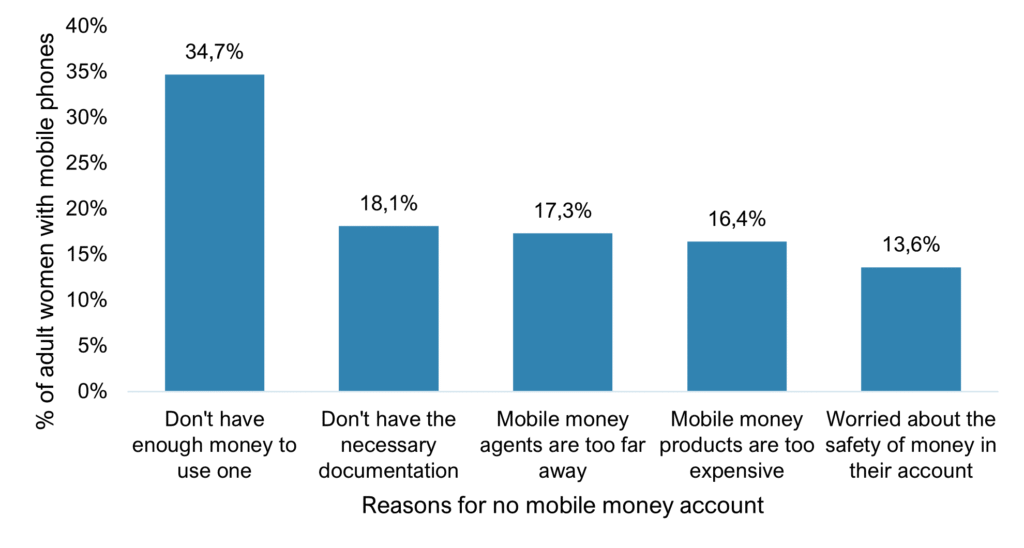

For many women, even if they have access to mobile phones, the combination of limited financial inflows and the cost of accessing digital financial services remains prohibitive, as shown by Figures 3 and 4 above. High account opening, maintenance and transaction fees may deter women from using these services. This pushes women to continue to rely on cash or informal options to meet their financial needs.

- Legal and cultural barriers are obstructing women’s account ownership

Almost 20% of women phone owners reported that they do not have a financial account because someone in the family already has one, implying that they use accounts owned by other members of the household, such as their husbands, for their financial needs. In some countries, laws and/or social norms play a role. According to the AfricaNenda 2023 SIIPS report, women in Cameroon, Chad, Equatorial Guinea, Eswatini, Guinea-Bissau, and Niger are legally prohibited from opening a bank account without their husband’s permission. Even where there are no legal restrictions, gender norms, such as the belief that women should not have financial privacy or personal savings, significantly restrict their financial decision-making and control.

- Financial services are not meeting women where they are

One of the main arguments made for digital financial services is that they break down proximity barriers. Yet 15% of women with mobile phones reported not having an account because financial service providers were too far away from them and17% stated the distance of mobile money agents was a barrier to having a mobile money account. Just having a mobile phone therefore does not mean that distance is no longer a barrier – human interaction is still valued, and in fact is a must as long as people continue to rely on cash-in-cash-out services in the absence of a full digital transaction ecosystem. There might also be gender-specific factors at play, such as the fact that women’s childcare and household duties make it difficult to travel to financial service points. CGAP’s gender norms report confirms that such gender factors are all too real.

- Having an ID is still not enough

Though at least 70% of women across all SSA regions have a form of ID, which enables them to register for a financial account, 18% of women in SSA with mobile phones highlighted a lack of necessary documentation to be a barrier to mobile money account ownership and 12% for account ownershipAccording to AFI, address verification has been particularly burdensome for women. In many cases, women’s names are not on residency documents, but rather those of the head of the household, often their husbands.

What needs to happen to bridge the gap

Mobile phones have facilitated digital financial inclusion for millions of women in SSA. However, having a phone is not a sufficient condition to get women to adopt and use DFS as long as other barriers prevail. This calls for particular attention on how to bridge the access and usage gap for women with phones as a “low-hanging fruit” target market for DFS.

Thought pieces and policy papers like CGAP’s recent blog on women’s usage, the G20’s GPFI recommendations on advancing women’s digital financial inclusion, and the W20 2025 Communique have all called for policy and market action to alleviate systemic barriers, promote innovation and use gender-disaggregated data to drive women’s access to and engagement with digital financial services. Our reflections above support this call to action:

- Design around women’s realities. Lack of money and distance remain key barriers for women, and one size fits all solutions have, so far, not been enough to breakthem down. Mobile money providers and fintechs are uniquely positioned to tackle this challenge by designing affordable products that fit women’s contexts, but this requires designing around women’s realities. This will require digital financial service providers to do targeted and nuanced research to understand this niche segment’s pain points in accessing financial services. Leveraging gender-disaggregated data, as already advocated by others, represents an important first step.

- Drive women’s autonomy in digital finance use. The Findex data indicates that many women may be sharing accounts with other household members, or may not have any account because somebody in the household already has one. To drive women’s autonomy, it is crucial to empower women to open and manage their accounts independently. Some of this can be solved through targeted awareness campaigns to highlight the benefits of personal accounts. But other barriers, such as removing any remaining gender-discriminatory legal restrictions, or addressing societal gender norms that disempower women’s financial autonomy, require systemic policy interventions..

In our next blog, we delve deeper into consumer outcomes, offering a nuanced reflection on women’s vulnerability in DFS and the implications for policy and product development from a consumer protection perspective.