Financial Inclusion

Making consumers interoperable: Biometrics and financial inclusion in sub-Saharan Africa

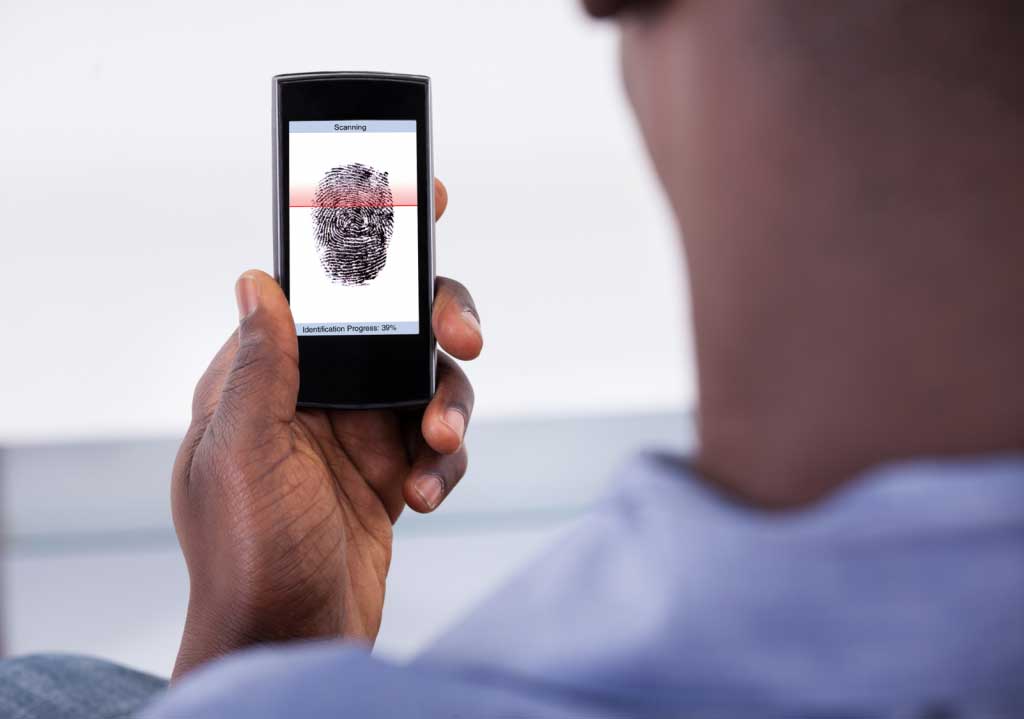

A recent study by the World Bank shows that as many as 1.1 billion people live without basic proof of identity. Being able to prove one’s identity is an important enabler in society. It allows one to access critical services, such as health services, government grants and education. It is