Why are women more vulnerable to risk in digital financial services?

Why are women more vulnerable to risk in digital financial services?

23 February, 2026 •This blog was written as part of GIZ’s Governance of Digital Finance project. Blog 2 of 3.

In our previous blog, we noted that despite increased access to mobile phones and identity documentation (IDs), women in sub-Saharan Africa remain less likely to hold a formal financial or mobile money account. Data from the 2025 Findex report identified limited affordability, a low value proposition, and distance of financial institutions and mobile money agents as key remaining barriers.

However, the data also highlights a less visible constraint. Among women with mobile phones, low trust (13%) and safety concerns (13.6%) were cited more frequently than documentation (11.5%) as a barrier to formal account ownership. This suggests that trust and vulnerability play a critical role in digital financial services (DFS) uptake among women.

While DFS risks affect all consumers to some extent, they are often more acute for women. This blog explores why this is the case and how regulatory and provider interventions can mitigate these risks.

How are women uniquely vulnerable to DFS risk?

World Bank research on financial consumer protection (FCP) and digital finance indicates that women are more vulnerable to DFS risks than men. Although this vulnerability is partly associated with lower levels of financial and digital literacy, shaped by gendered social norms that can constrain women’s confidence and limit engagement with financial services, these alone do not fully explain the disparity.

For example, even in societies like Kenya or Japan, where women often play a central role in managing household finances, research indicates they are still more vulnerable to DFS risks and fraud (see evidence from Kenya and Japan). This points to additional gender-specific factors that increase vulnerability, including among women who are otherwise financially active.

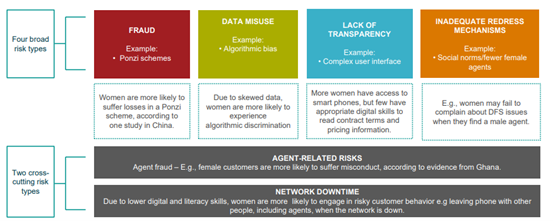

CGAP’s DFS consumer risk typology framework identified 66 risks and categorised them across four broad risk types, as shown by Figure 1 below. These are fraud, data misuse, lack of transparency, and inadequate redress mechanisms. Additionally, it identified two cross-cutting risk types that disproportionately affect women: agent-related risks, such as agent fraud and discrimination, and network downtime-related risks.

Without appropriate consumer protection and effective recourse that is applied with a gender and vulnerability lens, women may reduce their usage of, or altogether avoid, DFS for fear of being victimised. This risks reversing recent gains in financial inclusion.

Cenfri’s qualitative consumer research for AfricaNenda’s 2024 State of Instant and Inclusive Payment Systems (SIIPS) across five African countries (Algeria, Ethiopia, Guinea, Mauritius, and Uganda helped us to identify women’s self-reported vulnerabilities and categorise them into four DFS risk types:

1. Concerns over fraud, coupled with low confidence in using DFS, undermine trust

Fraud has emerged as a significant concern across several markets, especially for women respondents. For example, 64% of respondents surveyed in Guinea and 51% in Uganda reported being victims of fraud. In Uganda, concerns about fraud affected women’s trust in DFS, making them resort to using cash.

“Digital payment are dangerous because people can easily steal my money, that’s why I don’t normally use such I prefer cash.”

—Female DFS non-user, Uganda

In Ethiopia, women perceived themselves as more vulnerable to fraud and scams. Similarly, in Uganda, women reported that word of mouth and media reporting on fraud incidents make them hesitant to trust DFS, particularly if they already don’t feel confident using DFS:

“I am fully inclined to using cash and do not use digital payments at all. The reason is because I fear using digital payment methods that I am not familiar with. I am however aware of the benefits, but I do not know how to use them.

—Female DFS user, small business owner, Ethiopia

2. Data misuse

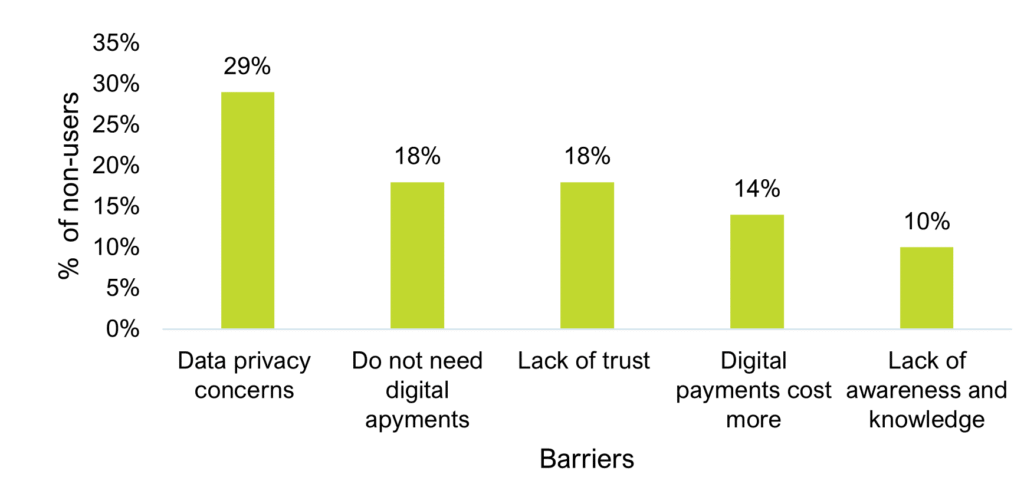

Data privacy concerns were among the most frequently cited barriers to early of DFS by consumers across the case study countries (men and women alike). Figure 2 below shows that nearly three in ten non-DFS users (29%) cited data misuse as a deterrent to using digital payments. However, our research for AfricaNenda revealed that this challenge is particularly acute for women. For example, in Mauritius, women reported that they felt more vulnerable than men to data privacy violations.

3. Lack of transparency coupled with lower literacy levels undermine women’s agency

When DFS providers do not clearly communicate terms, conditions, fees, and features of their financial services to consumers in a way that they can easily understand, consumers become more distrustful of DFS for fear of being “cheated”. According to MicroSave, women are more susceptible to risks associated with lack of transparency on product features, fees, and other terms and conditions when they rely on agent assistance and family to make transactions.

These risks include overcharging, hidden fees, mis-selling, and over-indebtedness. For example, in Guinea, women were found to have lower literacy levels than men, making them more reliant on others and likelier to make mistakes. :

“My wife hasn’t studied. If she wants to send money to her mom, she must go through me because she can’t read very well”

— Male DFS user, Small enterprise owner, Guinea

It is incumbent on DFS providers to ensure maximal transparency when engaging with consumers, particularly those with limited literacy skills, as these consumers are the most vulnerable to this risk.

4. Access to effective consumer redress mechanisms remains a barrier for women

Not all DFS risks can be completely prevented: human error, circumstances beyond the DFS provider’s control, and the evolving sophistication of criminality can circumvent the barriers put in place to protect users. However, robust redress mechanisms and accessible, supportive customer support play a crucial role in ensuring women can confidently seek recourse to recover losses and continue using DFS safely.

Yet, in our qualitative research, four of the five markets studied identified poor customer support as a key barrier to recourse. This includes unclear support channels or slow customer service Women are more impacted by this: their lower experience of DFS usage, as well as their more limited voice and agency in some societies, directly impacts their confidence to seek out redress and submit complaints. A CGAP study in Cote d’Ivoire showed that women were 10 percentage points less likely to reach out to seek recourse with their providers and five percentage points less likely to know how to do so. Agents were also reported to be nine percentage points less likely to address a woman’s complaint.

The following quote from the SIIPS consumer research in Algeria poignantly illustrates the frustration that many women face:

“We never know really to whom we can complain or get information from, everything is not clear.”

—Female DFS user, Algeria

Intentionally integrating women’s DFS risk vulnerability into consumer protection

Instituting sound financial consumer protection frameworks is key to addressing DFS risks, protecting consumers, and ensuring meaningful consumer outcomes.

Unlike traditional rules-based frameworks, principles-based frameworks effectively adapt to the ever-evolving risks in DFS as new trends and technologies emerge. However, greater nuance is required to ensure that the most vulnerable consumers, including women, receive the right level of protection needed to meaningfully engage with DFS. A solution could include offering women customers the ability to opt-in and out of data sharing so they have full control over their data privacy. Women-specific solutions can include using plain language in disclosures under terms and conditions or transaction notifications, particularly for women with low literacy levels. Additionally, increasing the number of female customer service agents to address women’s complaints and other issues, such as fraud or coercion, may be beneficial.

In a 2024 review for Consumers International of the regulatory responses to vulnerability around the world, we saw that there’s no universal definition of what constitutes vulnerability. Consumers may be vulnerable due to personal characteristics (such as gender), circumstances (income, literacy, or caregiving responsibilities), and/or the nature of DFS products they use.

For women, these intersecting factors compound their risk profiles. For example, CGAP’s report on DFS consumer risks shows that low-income women and particularly those in rural areas, are uniquely more exposed to DFS risks. Therefore, a one-size-fits-all approach won’t do – the future of consumer protection requires financial institutionsbe held accountable for the outcomes of consumers, taking into consideration their unique personal circumstances and risk profiles. The research quoted in this blog suggests that once women’s vulnerabilities are considered and incorporated into DFS products and consumer protection, women’s consumer experience will improve, and trust will follow.

This is a tall order. So where do we go from here?

It starts with better data and a different design mentality

Much has been written advocating for better use of gender-disaggregated data (GDD) in policymaking and driving market practices. By implementing effective monitoring protocols, regulators and industry can identify and minimise bias in their internal processes and algorithms. Additionally, they can ensure approaches are better tailored to women through SDD and GDD, making the gendered impacts of DFS risks more visible and enabling FCP measures to be tailored to women-specific vulnerabilities, such as those described above. Importantly, effective monitoring would allow regulators and industry to hold markets accountable for outcomes for women, rather than focusing solely on compliance inputs.

Having more gender-disaggregated data is of little use if it doesn’t feed into clear regulatory and market use cases. Regulators and industry providers need to view women’s experiences and vulnerabilities as core design inputs. This includes systematically integrating a gender lens into supervision, market conduct rules, product design and complaints analysis.

If we want to unlock the value of DFS for driving greater financial inclusion, and ultimately greater economic empowerment and overall wellbeing for women, then stronger, gender-intentional consumer protection must become the norm, not the exception. Now is the moment for regulators and providers to step up and make that a reality.

In our next blog, we delve into understanding the financial needs of women MSMEs, reflecting on our study on women cross-border traders in SADC to understand the pain points they experience in financial services, particularly from a cross-border trade perspective.