5 lessons for designing fit-for-purpose health microinsurance

5 lessons for designing fit-for-purpose health microinsurance

31 January, 2023 •Gakere is a 49-year-old mechanic from Nairobi, and like 77% of adults in Kenya, he does not have National Hospital Insurance Fund (NHIF) or private health insurance.

“If I fall sick, I treat myself. As you can see I do very strenuous jobs and someone who does not have good health cannot do this job,” he explained, “Here at my work place I can get injured and my employer can disown me in case I get injured but if I have a health insurance it can be able to help me [sic].”

Many Kenyans are like Gakere – they are uninsured and thus not equipped to cope with unexpected medical risks and the associated costs. As a result, they will often have to pay high out-of-pocket fees if they want to access care at private facilities and are likely to resort to a variety of informal fundraising mechanisms to pay these fees.

Health microinsurance (HMI) has the potential to bridge the health insurance gap in Kenya. With funding from Swiss Capacity Building Funding (SCBF) and technical support from Cenfri, Britam and M-TIBA has been working to scale up their low-cost, mobile-based, retail HMI solution in Kenya.

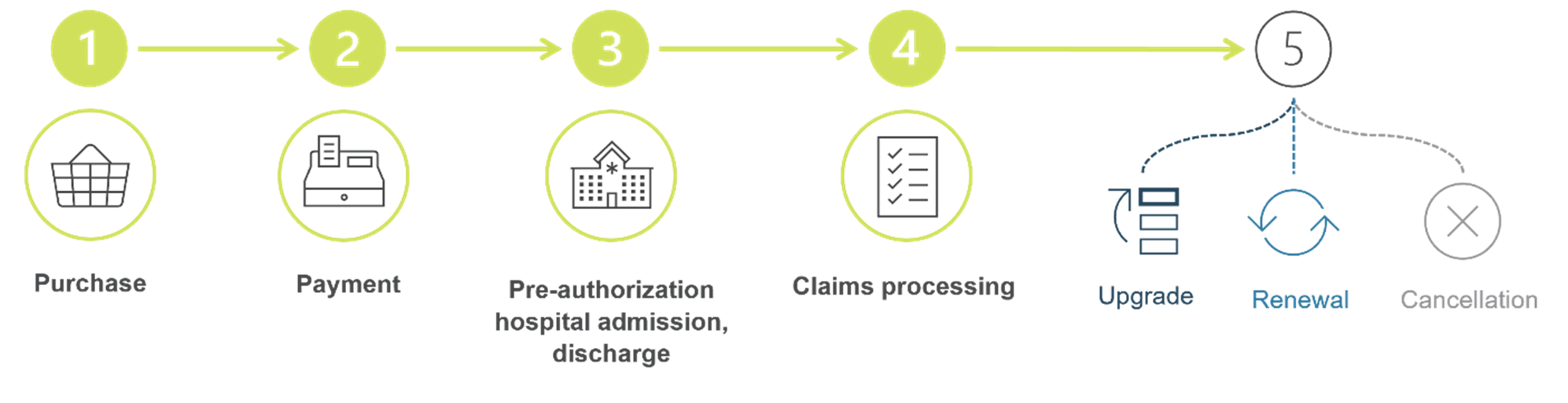

The initial stages of the project included two phases of qualitative research. In the first phase, we sought to understand the needs of M-TIBA customers, while the second phase centred on understanding how the customers of the Britam M-TIBA HMI product experienced the customer journey, as illustrated in the figure below. Purposive sampling was used for both phases of the study to ensure that there was balanced sample by age and gender, and a fair representation of respondents from both urban and rural areas.

Based on insights from on-the-ground consumer research in Kenya, five lessons have emerged for microinsurance providers in sub-Saharan Africa (SSA) to make their insurance value proposition work for this target market.

1. Value is the name of the game

It is well known that low-income consumers are price sensitive, however our findings in Kenya are a little more nuanced; low-income consumers are very value sensitive as well. They need to budget wisely and stretch their income as far as they can, but they are willing to pay for products that are perceived to offer them good value-for-money. This extends to bundled offerings too. Clients also expressed a desire for funeral cover and bundling other Britam offerings to their HMI. The focus for nearly all HMI consumers is whether the benefits would help meet their unique expectations around coping with medical costs. Therefore, bundling and even upgrading offerings to meet these needs is desirable to these consumers, as long as it is perceived as adding value.

2. Make a good first impression

It’s important to take care in the customer onboarding process. A positive engagement with a sales agent early on shapes one’s experience of the whole customer journey. Clients that felt that agents had taken the time to explain products to them and given them time to consider their purchase reported fewer issues with the customer journey and reported a higher perceived value of the health insurance product, compared to those that had a quick onboarding with little explanation or attention paid to them. In line with lesson 1 above, if it is perceived to be adding value, clients are more likely to renew or even upgrade their health insurance.

3. Simplify, simplify, and then simplify some more

There is a limited understanding of how insurance works – both among those that have and don’t have insurance. Clients complained of complicated paperwork and hard to understand Ts&Cs. Simpler communication is needed that enables consumers, especially those with limited financial literacy, to understand and compare HMI products. Plain language that communicates the terms and conditions clearly is an essential characteristic of a simple product because it helps the consumer understand how the product meets their needs and can mitigate any misconceptions around an insurance product.

4. Digital is great, but the human touch is still important

Clients appreciate communication, especially with a real person. While a number of clients stated that they found the digital reminders to pay for their premiums helpful, they also enjoyed the “human touch” of being able to speak to someone if they had a problem. These principles can be applied to other aspects of the journey that consumers had trouble with. For example, reminding clients where their nearest networked hospital is (this can also be used as a nudge for clients to update their residential address). Good microinsurance products can fail because of poor distribution, but, conversely, strong distribution channels can lead to significant uptake of a less optimal product. Channels that facilitate a two-way discussion between consumers and the product’s representatives give consumers a chance to understand a product better. While digital channels are effective in reaching people, it is important to have a human touchpoint to provide a face to the product, thereby building trust and assisting consumers who lack access to digital channels.

5. Partners impact perceptions

Some Britam M-TIBA clients who were interviewed reported that they were admitted to hospital and attempted to claim from their insurance but experienced problems, because partner hospital staff were unfamiliar with the insurance product. This was due to high attrition among the hospital front desk staff and some trained staff had left the hospital. In this instance, clients’ experience was affected – highlighting the importance of the entire health-insurance value-chain. Therefore, it is important that hospital front-desk staff are regularly trained and kept up to date with details of the insurance coverage so that clients have a positive claims experience.

By deepening our understanding of the market’s perceptions of insurance, sentiment about the hospital industry and current resilience practices, we have started to identify ways that Britam’s HMI product could be adapted to reach more of the low-income market segment. The next phase of our work will be to make adjustments to the product and customer journey based on these recommendations. The intention is to improve the actual and perceived value of the product for current and potential clients, thus increasing client retention and policy renewal, and also hopefully growing the market.

After these changes have been implemented, we intend to conduct more qualitative user-experience research to test the new product features with clients and observe if the customer journey has in fact improved. Addressing the issue of health financing in emerging markets will not be easy; but products that seek to account for a customer’s needs as well as customer journeys that are deliberately designed to maximise customer satisfaction, engagement and understanding are a step in the right direction.

If you would like to read more about our work in microinsurance and health financing you can find it here and if you are interested in working with us, you can contact Rose Tuyeni Peter.